Commercial Crime & Fidelity Bonds: Protecting Your Business from Internal Fraud

Key Takeaways

- Most companies in Bangalore have a blind spot for internal fraud, and you won’t get coverage for employee dishonesty with your standard property or liability policy.

- Fidelity bonds cover losses due to employee theft, forgery and embezzlement. Commercial crime policies go a step further to cover things such as third-party fraud and funds transfer scams.

- The highest exposure is in IT, fintech, retail and logistics companies, given the high volumes of transactions and access-based roles.

- That depends on how many of you there are, how many assets your team manages and how good your internal controls are.

- A broker will help you compare insurers, sort out the right limits and push claims through without resistance.

Why Internal Fraud Belongs on Your Risk Register

You probably spend most of your risk budget on cyberattacks, compliance fines, and market shocks. Meanwhile, the bigger threat often walks into your office every morning.

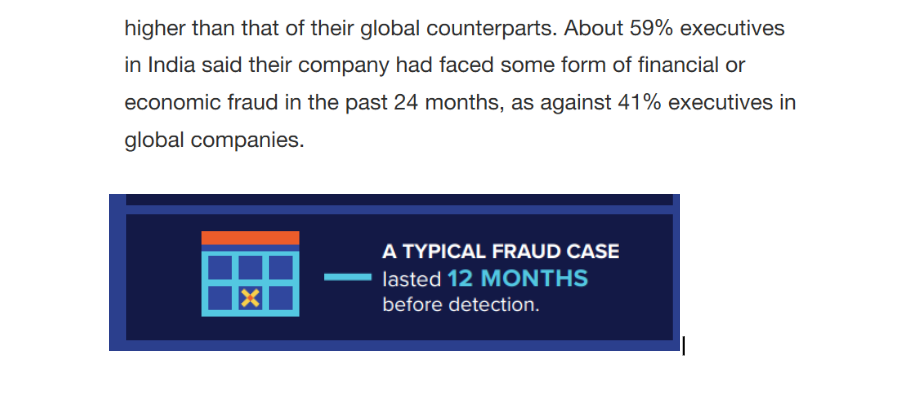

59% Indian organisations surveyed in the PwC India Economic Crime Survey had been victims of fraud in recent years, and many of these cases involved internal staff. For a fast-growing Bangalore company, one such incident can eat up months of profit. And these schemes usually run for over a year before anyone notices.

That is where commercial crime and fidelity bond insurance step in.

What a Fidelity Bond Actually Pays For

A fidelity bond, also called employee dishonesty cover, reimburses your business when staff cause direct financial loss through dishonest acts. It is a safety net for trust-based roles.

In India, a standard fidelity bond responds to:

- Theft of cash, securities, or inventory by a permanent or contract employee

- Falsification or alteration of checks, drafts or financial documents

- Falsification of accounts, payroll or expense reports to embezzle

- Computer fraud where staff transfer funds without authorisation

The policy pays the actual amount stolen, plus reasonable investigation costs. You can structure it on a named-employee, position, or blanket basis. For most growing firms, blanket cover is the cleanest option.

Where Commercial Crime Cover Goes Further

Commercial crime insurance builds on the fidelity base. While fidelity bonds focus on your own people, crime policies also respond to outsiders who exploit your systems or trick your staff.

A commercial crime policy usually includes:

- Third-party fraud, such as vendor invoice scams or CEO impersonation

- Funds transfer fraud from fraudulent payment instructions

- Social engineering losses where employees are duped into wiring money

- Counterfeit currency or securities accepted in the ordinary course of business

If you run a SaaS firm in Whitefield handling client billing, or a retail chain in Koramangala managing daily cash, this wider net matters.

Sectors That Cannot Afford to Skip This

Not every business carries the same exposure. But these sectors should treat fidelity and crime cover as essential, not optional:

- IT and SaaS firms: Employees with admin access to client billing or payment gateways

- Fintech and lending startups: High transaction volumes and KYC-sensitive data

- Manufacturing and logistics: Inventory shrinkage, fuel theft, and procurement kickbacks

- Retail and F&B chains: Cash handling across outlets with thin oversight

- Professional services: Trust accounts, client funds, and payroll exposure

Consider a familiar pattern: a finance executive at a Bengaluru logistics firm sets up shell vendors and routes payments to a personal account. The scheme runs for 18 months and bleeds the company of crores. It surfaces only during a year-end audit. Without a crime policy, that entire loss comes straight out of working capital.

What Will Trigger a Claim, and What Will Not

Knowing the boundaries before you buy saves you grief later. A fidelity bond pays out when the dishonest act is intentional and causes direct financial loss. It is not built for honest mistakes, weak performance, or trading losses.

You can typically claim for:

- An accounts payable clerk creating ghost vendors

- A warehouse supervisor diverting stock for outside resale

- A senior staffer pushing through fake reimbursement claims for months

You usually will not get paid for:

- Losses discovered after the policy expires, unless you have run-off cover

- Indirect losses like reputational damage or lost business

- Fraud committed by directors holding a majority stake

This works much like other specialised policies. Our piece on product recall insurance explains how niche covers respond to specific triggers.

How to Pick the Right Policy

Matching policy structure to actual exposure is key to selecting the right cover. A practical way to handle this is:

- Map your risk areas: Identify roles with access to cash, inventory or sensitive data

- Set realistic limits: Base your sum insured on maximum single-loss potential, not average claims

- Check the retroactive date: Past acts discovered during the policy period should be covered

- Review sub-limits: Social engineering and funds transfer often carry lower internal caps

- Coordinate other policies: Avoid overlaps and gaps with your cyber and D&O covers

The IRDAI’s renewed focus on audit and governance also strengthens the case for cleaner risk transfer.

Final Word

Internal fraud rarely announces itself. It builds quietly, often through someone you trusted enough to hire and promote. A well-structured fidelity bond or commercial crime policy gives you the financial cushion to recover without disrupting operations or rattling investors.

At Edify Insurance Brokers, we help Bangalore businesses in IT, fintech, manufacturing and retail to craft crime and fidelity covers that are appropriate to their actual operations. Whether you want to review an existing policy or create one from scratch, our team can walk you through the options.

FAQ

- Is fidelity bond insurance mandatory in India? It is not legally required for private firms, but many client contracts in BFSI and IT services insist on it as a condition of engagement.

- How much is the premium? Insurers consider your industry, number of employees, internal controls, sum insured and claims history. SME premiums may start at a few thousand rupees a year for modest limits.

- Can I claim if the employee has already left? Yes, as long as the dishonest act happened while they were on your rolls and is discovered within the policy or discovery period.

4. Are contract or third-party workers covered? Standard policies cover permanent staff by default. You can extend cover to contractors, interns, and temps through a specific endorsement.